Pigou Lecture

Wednesday 10th May 2023

I wanted to deliver this lecture after taking part in a psychology elective. In the elective, we were given a couple of lessons to prepare a powerpoint on any aspect of psychology,

so I chose herd mentality and how it relates to the stock market. Having done this, I decided it would be good to present to the School's Economics society. I put together a couple more

slides with a friend and we presented it to around 30 people.

The Harrovian write-up

On Wednesday 10 May, Viktor Van den Berghe and Vlad Plyuschenko gave an illuminating talk on the topic

'Herd Mentality in the Stock Market' and how everyday investors can use their knowledge of this psychological

phenomenon in making smart investments in the stock market. To mix things up a bit, the speakers changed

the lecture structure slightly so that anyone could ask questions during the lecture to promote discussions

and debates on different concepts.

Attended by an immense crowd across all year groups, Van den Berghe first

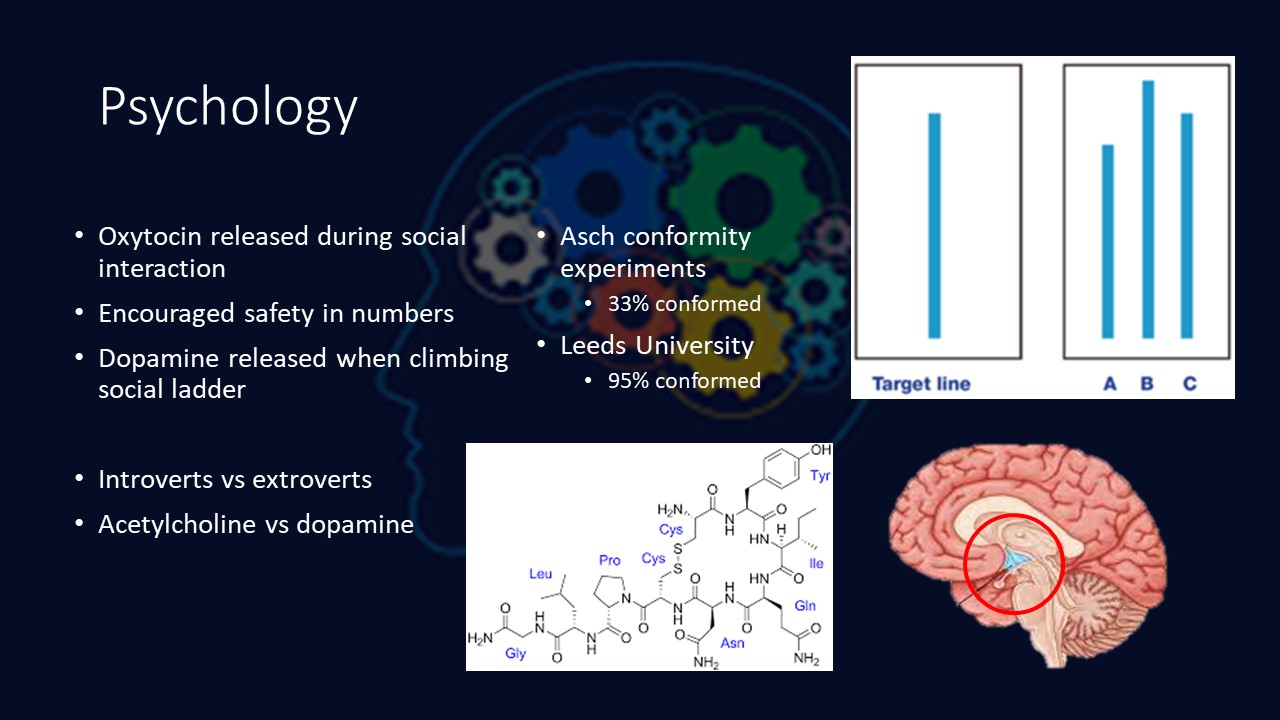

broke down herd mentality into its basic foundations, defining it as the 'tendency of people to confrom to the group

to which they belong' and broke down the psychological research explaining this unique phenomenon where there is the

release of oxytocin and dopamine during social interactions. Their addictive nature is what makes people willing to be

part of a group, thus leading to the behavioural phenomenon of herd mentality. However, he stressed that the impacts of

herd mentality vary across introverts and extroverts due to whether acetylcholine or dopamine reward systems are used.

Van den Berghe backed up these claims with psychological studies, primarily the Asch conformity experiments, and another

conducted by researchers at Leeds University. Borht researches yielded convincing results that strongly emphasise the powerful

nature of herd mentality.

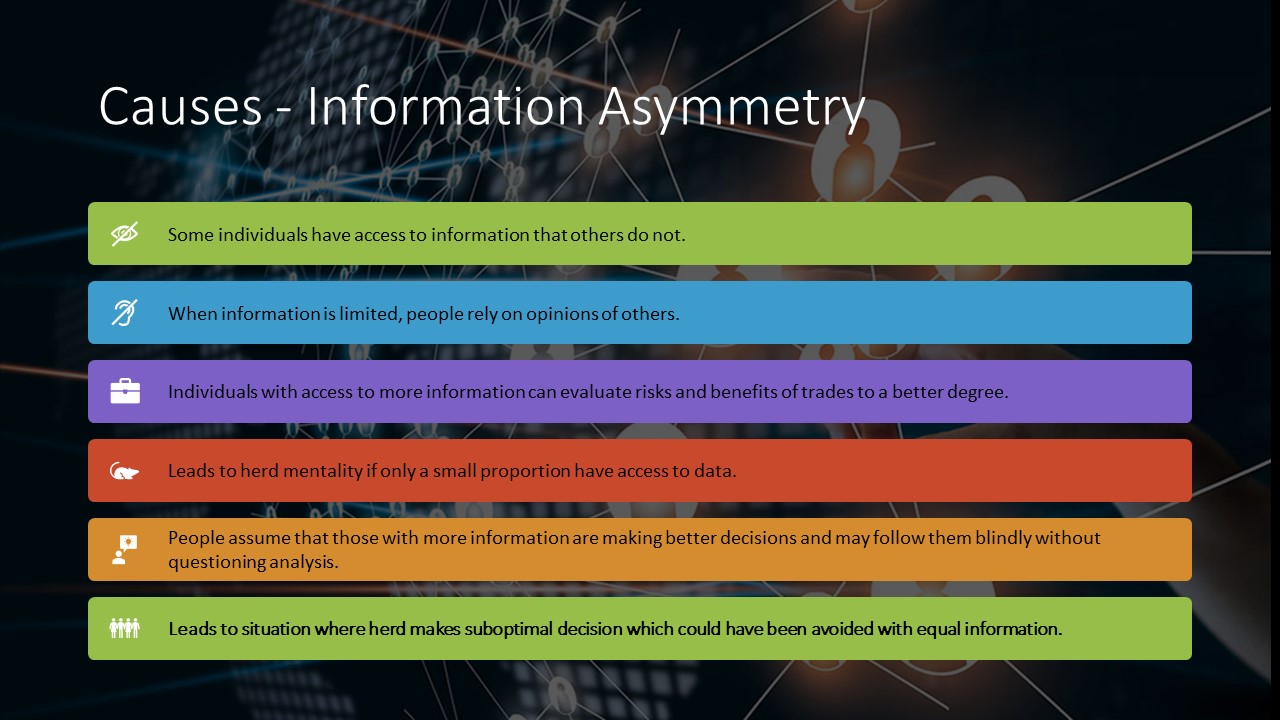

Plyuschenko then identified the main cause of herd mentality as information asymmetry, such

as the assumption that those with more information are better at making decisions and thus people may follow them blindly without

questioning their reasoning. This could lead to situations where the herd makes a suboptimal decision, which could be avoided with

equal information. Van den Berghe highlighted the adverse risks associated with this, such as the threat of normalising

risky behaviour and extreme views, which in turn can lead to the emergence of market bubbles, which is when the current price of an asset

greatly exceeds its intrinsic valuation.

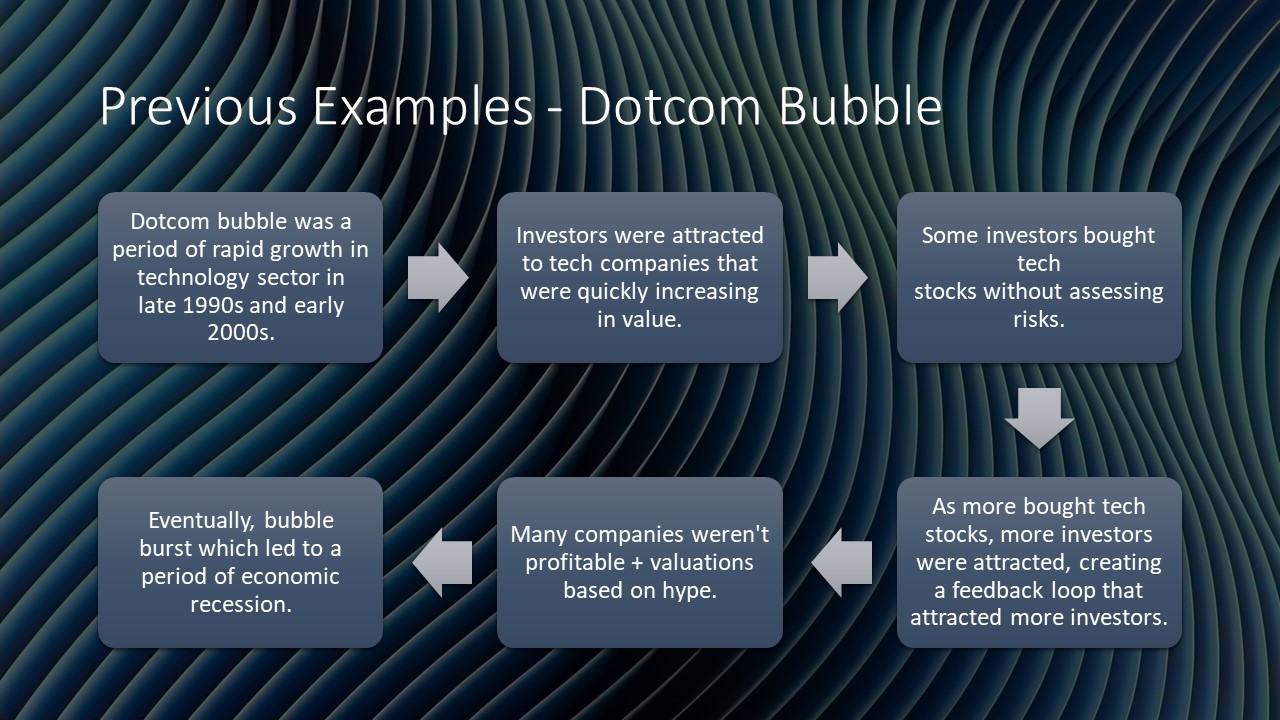

Next, Plyuschenko artfully described a textbook case study showcasing this: the

dotcom bubble. The dotcom bubble arose because investors bought tech stocks without assessing the risks due to the rapid expansion

of the technology sector in the late 1990s and early 2000s. More and more investors were attracted to the rising tech stock prices,

thus creating a feedback loop that attracted even more investors. However, many of the technology companies were not profitable,

and were being invested in because of hype. Eventually, investors realised this and bubble burst, leading to massive selloffs of stocks.

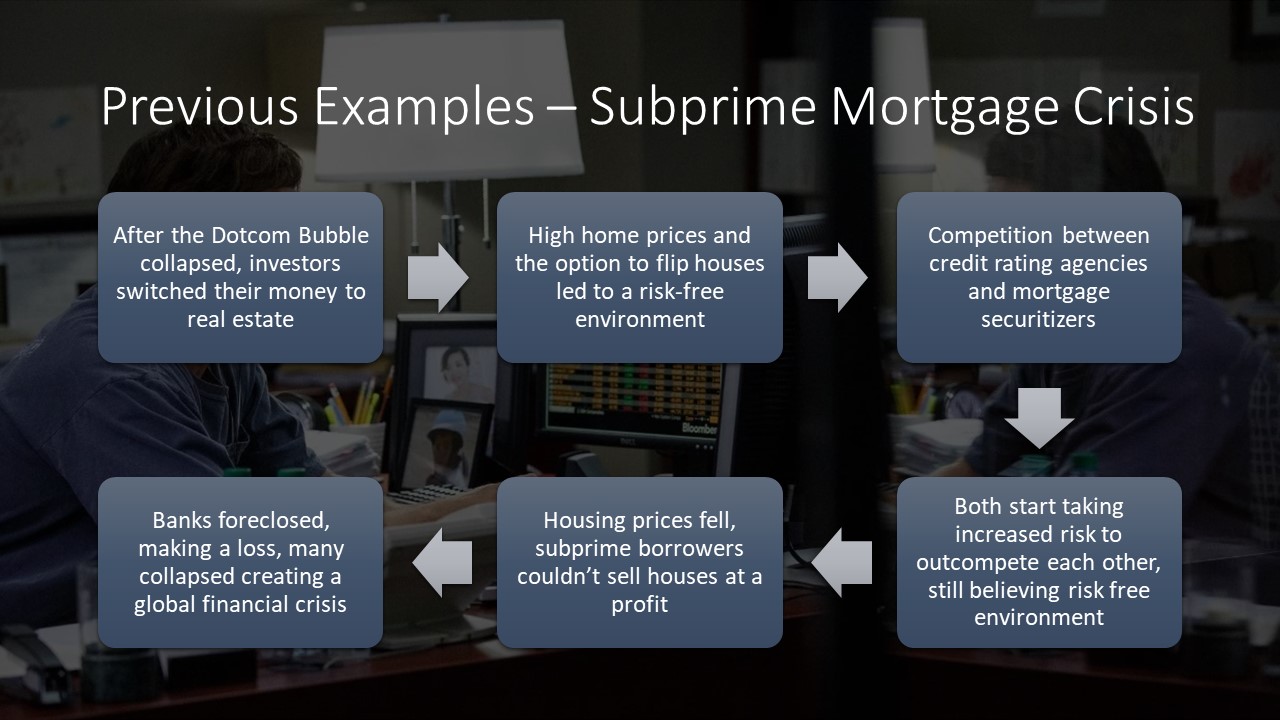

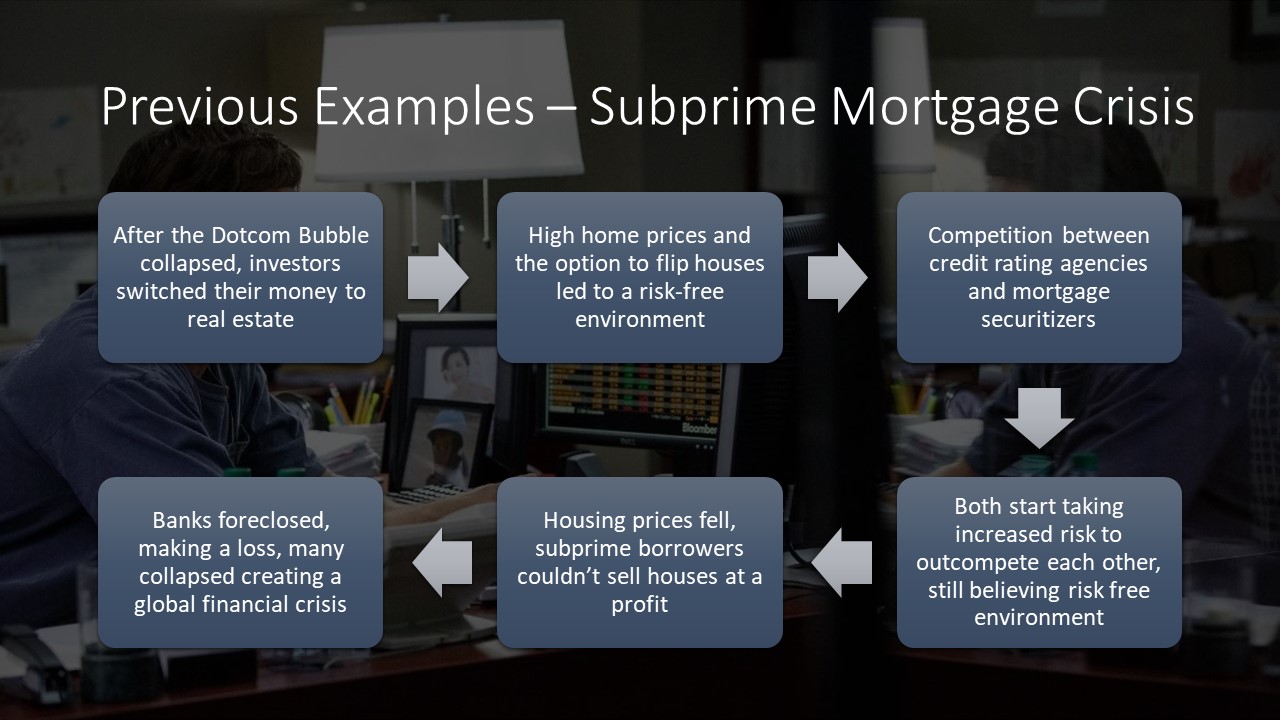

Van den Berghe proceeded to stress that the subprime mortgage crisis followed a similar pattern, where favourable, risk-free environments

arose from high house prices and the option to flip houses and residential real estate was generally seen as a safer investment. With rising

competition between credit rating agencies and mortgage securitisers, riskier and riskier loans were given out in attempts to outcompete

other firms. However, this all fell apart when the Fed increased interest rates, so real estate with adjustable-rate mortgages, particularly

the risky ones that should not have had such loans, could not make the increased payments and hence defaulted on payments. This led

to a systemic shock in the financial system, and eventually led to the infamous global financial crisis. To emphasise this point, Van den Berghe

and Plyuschenko broke up the lecture with a fascinating clip from the movie The Big Short, which highlighted Van den Berghe's

point and reasoning behind how the subprime mortgage bubble rose.

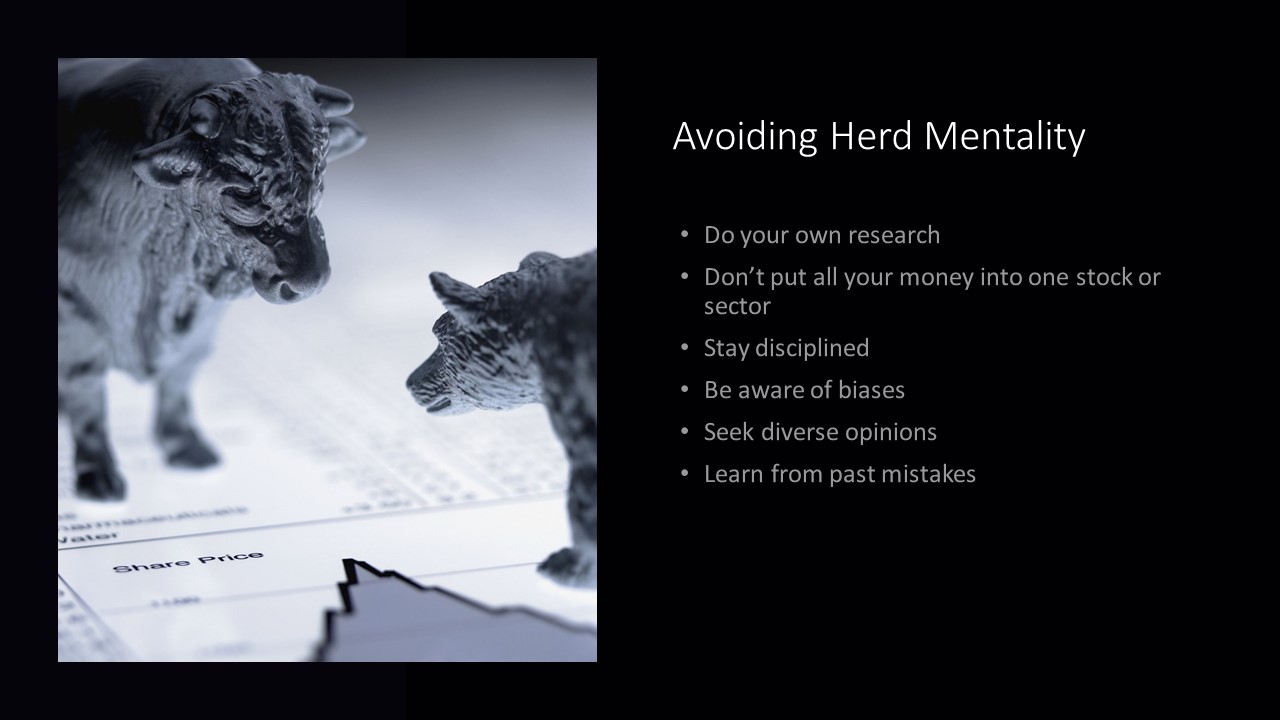

After this, Plyuschenko provided advice on avoiding herd

mentality, emphasising the importance of research, being aware of biases, learning from past mistakes and seeking diverse opinions. Thereafter,

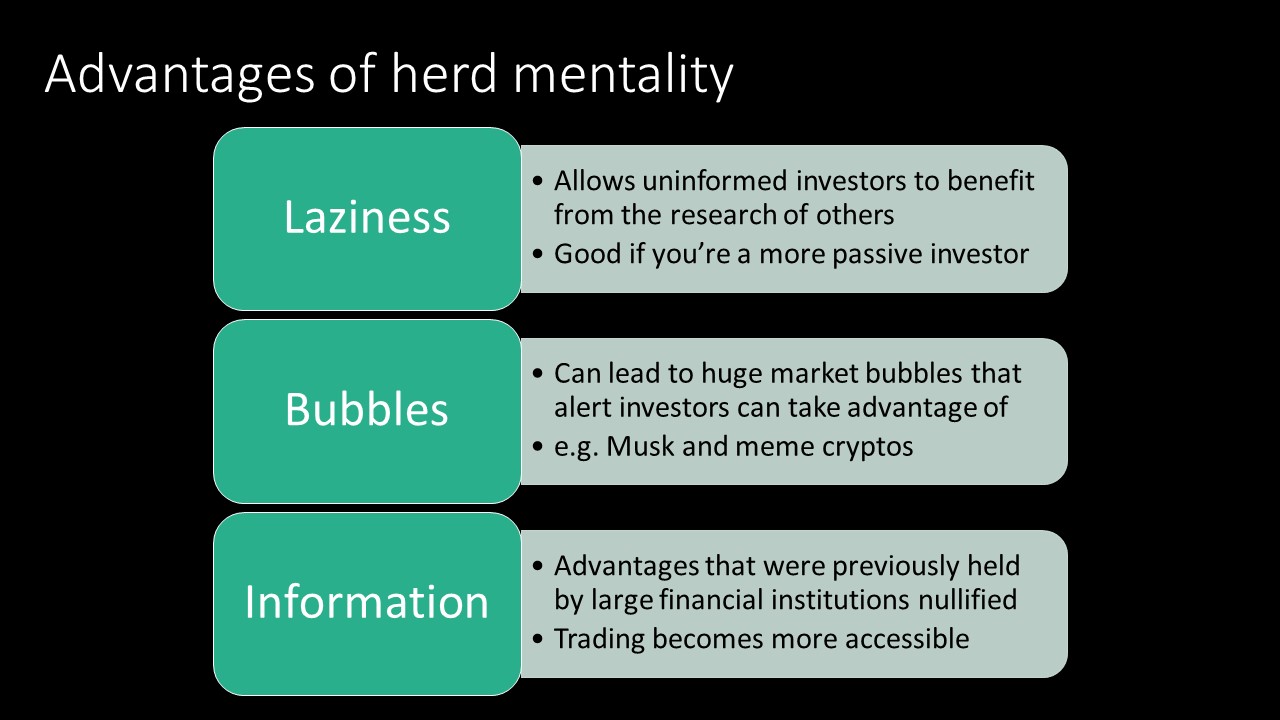

Van den Berghe suggested how investors could take advantage of herd mentality, as it promotes lazy trading by following the advice of others,

and investors can take advantage of huge bubbles, such as the 600% rise in price of GameStop for no reason at all.

Plyuschenko

finished the lecture by highlighting some emerging trends in the stock market that exacerbate herd mentality, particularly algorithmic

trading, where computerised methods of buying and selling stocks could lead to market instability but he did emphasise the ethical

implications of this new method of trading, where there are unfair advantages for those who can buy these advanced technologies and

benefit from it.